June is here! 🌞 Here’s a summary of the Fairfield and Westport CT single-family markets in May 2026 compared to a year ago.

May 2026 Takeaways 📝

Inventory was still low but was rising.

On average, homes sold 3-5% over the asking price, but this average reflects a wide range.

Some homes sold way over asking with bidding wars and others sat on the market, or had price reductions.

Market time was up in both towns.

Buyers need to work with their agents to determine the best way to approach an offer based on the conditions specific to the home of interest, since competition is case-by-case.

Sellers must approach the market strategically to capitalize on buyer demand balanced with buyer fatigue and be perceived as the best value available for the price.

If you are financing, your offer needs to be extra attractive because you may be competing with cash offers that are very attractive to sellers due to their simplicity. As much as 46% of the May sales were cash deals in Westport, and 28% in Fairfield.

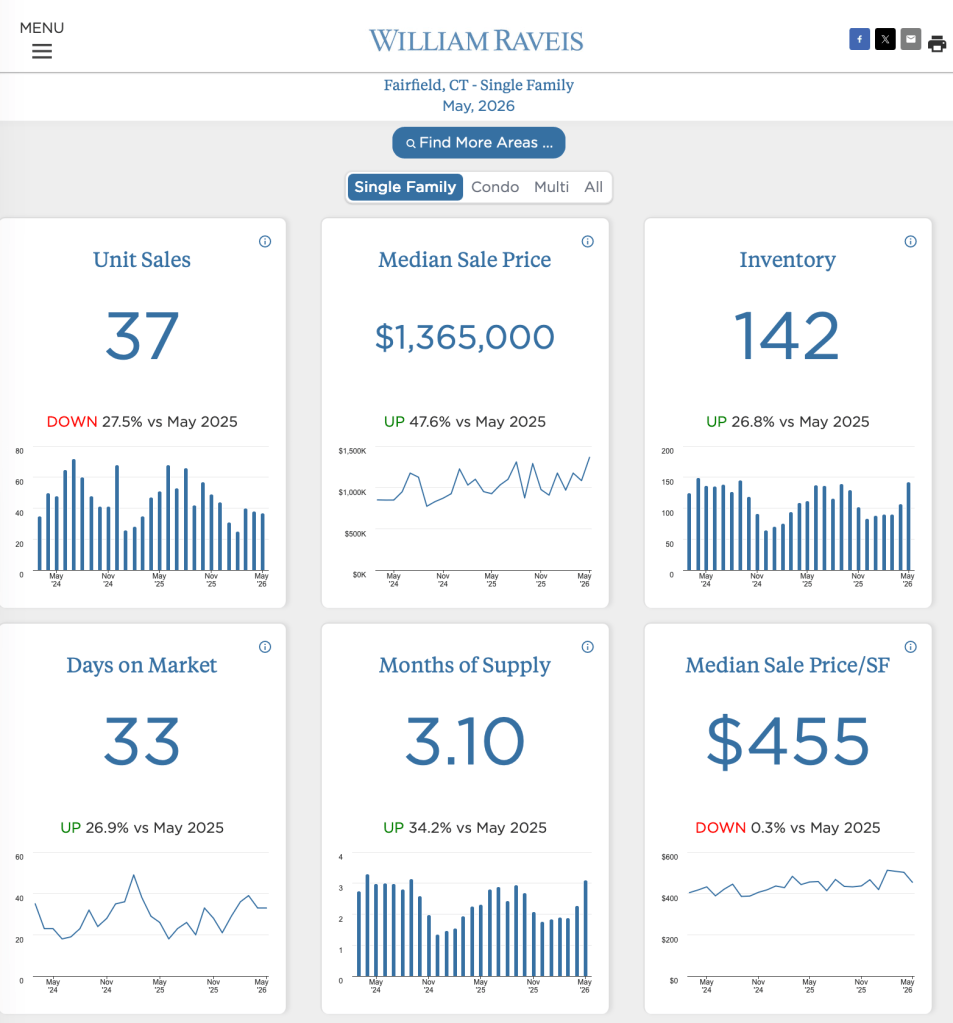

In Fairfield, sales were down 28% from last year, while inventory was 27% higher. The housing supply increased to 3.1 months-worth in May. These factors were helpful for buyers, though the median sale price was way up, 48%, compared to last May. Market time was longer than last May with an average of 33 days to contract, and 11% of homes took 90 days or more to get a signed contract.

Homes sold for an average of 105% of the asking price. This reflected a huge range though, from 79% to 138% of the list price! Most homes sold close to full price, with 86% of homes selling at or above 95% of the list price. Cash deals accounted for 28% of the sales, significantly fewer than last month.

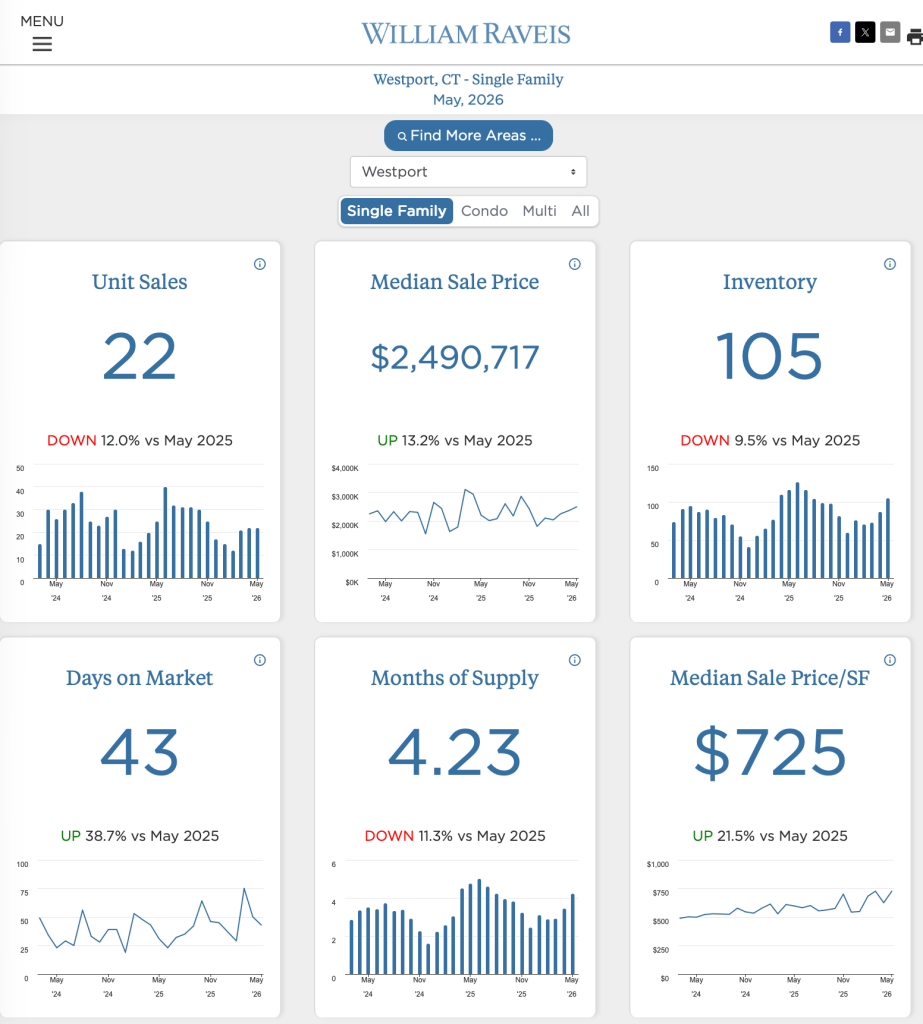

Sales and inventory were down in Westport, compared to May 2025. The months of supply metric was also down to 4.23 months, though this reflected an increase from last month. Days to contract averaged 43, which was a significant increase from the prior year, though fewer than last month.

Sale prices averaged 103% of asking. There was also a wide variation here, with a low of 94% up to as high as 121% of the price. Ninety-one percent of the sale prices were at or above 95% of the asking price. Forty-six percent of the of the buyers in May reported using cash. A number of buyers withheld this information, so the percentage could be higher.

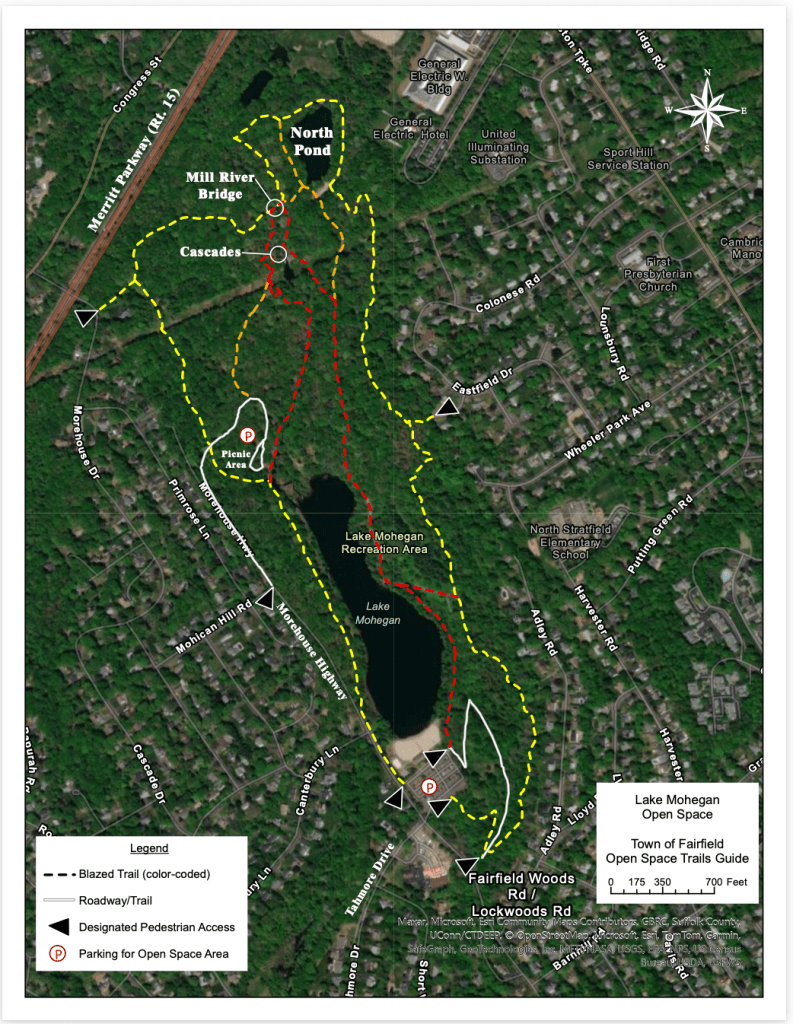

The streets near Lake Mohegan have a relaxed peaceful vibe. Neighbors are friendly, and many embrace an active lifestyle, so you can expect to see people out walking. Residents especially love to take advantage of living near the lake. With the beautifully scenic and peaceful trails, the Cascades waterfall, the natural dog beach, life guard staffed fresh-water swimming beach, and the playground and Splash Pad sprinkler area for kids, nearby home owners embrace the lake area lifestyle and enjoy it all!

How good are the schools? 🎓

Fairfield is known for top-rated schools at all levels, and the North Stratfield Elementary School in the neighborhood is award-winning. Many families with children are attracted to Fairfield and the neighborhoods near Lake Mohegan for this reason.

Can you actually use Lake Mohegan year-round? 📆

Yes, the open space at Lake Mohegan is actively used year-round. There are two marked trails for walking, hiking, picnicking, and outings with your dog. Fishing is permitted along the shoreline. The beach and sprinkler areas are seasonal. Lake Mohegan is one of the most popular recreational outdoor spaces in town. Access to the trails and the parking lot are free to the public.

How dog-friendly is it? 🐕

Very! The trails and dog beach are perfect for dogs. Once you get about 100 feet from the parking lot, dogs are even allowed to be off-leash. Dogs are not allowed in the public swimming, pavilion, or sprinkler and playground areas, but the rest of the 170-acre open-space park is exceptionally dog-friendly. Below is the open space trail map from the town of Fairfield.

What’s the commute to NYC? 🚊

Manhattan is 61 miles from Lake Mohegan, and most commuters take advantage of the convenience of the Metro North Train. The Fairfield Metro is 3.7 miles and about 11 minutes by car.

Are home prices still rising? 🏷️

Home prices throughout Fairfield continue to experience upward pressure due to high demand and limited inventory. At the time this is written (6/7/26) there are 91 homes for sale in Fairfield, and just three in the Lake Mohegan neighborhood.

How does it compare with beach-side of Fairfield? 🏖️

You can expect to get more property and privacy for your money in the Lake Mohegan neighborhood. Most properties here are in the R-3 residential zone with property sizes of .45 of an acre or larger. The Fairfield beach area is comprised of homes primarily in the A and B zones with .21 of an acre or less. Most of the homes in the Fairfield Beach area are in the AE Flood Zone and are subject to flood insurance and special building requirements. Lake Mohegan and Jennings Beach on Long Island Sound are 5-6 miles apart, which is 15 to 20 minutes by car. Whichever neighborhood you choose, these fabulous natural resources are not far away!

Are there flood issues? 🌊

The lake and nearby Mill River are situated in a deep valley with nearby homes occupying property at a significantly higher elevations. Run-off from heavy rains tends to flow toward the lake rather than pool on the streets. Properties near the lake are in the low-risk risk zone on the flood maps, and flood insurance is rarely required. Storm surges from the Long Island Sound are too far away to impact this area.

Is there enough nearby shopping and restaurants? 🛍️ 🍽️

There’s an abundance of shopping, restaurants, and amenities on Black Rock Turnpike, which is about five minutes and under two miles away. An additional hub of shopping and restaurants is located in downtown Fairfield, about 12 minutes and 4 miles away by car.

What do current residents like most? 🤗

Nearby residents love that they can walk to the Lake Mohegan trails, Cascades waterfall, hiking trails, fishing spots, and the fresh-water swimming beach. They value the rare opportunity to be surrounded by nature with the convenience of being just minutes to shopping and dining, the Merritt Parkway, I-95, and the train. They enjoy access to top schools. And they cherish owning more land that offers privacy and plenty of space for recreation and gardening, in a neighborhood with an all-around “vacation-at-home lifestyle”!

Questions or comments about the Lake Mohegan neighborhood? Send a note below.

With Fairfield and Westport Connecticut real estate markets favoring sellers since 2020, it’s easy to assume that every home magically flies off the shelf. The reality is that the homeowners who seek a savvy agent, align with the strategy they propose, and take advantage of the resources they provide are the ones who enjoy success!

Every successful sale is the result of more than marketing alone. It begins with a shared commitment between homeowner and agent, followed by strategic planning, careful preparation, and ongoing collaboration throughout the process.

Aligned Vision

We met to confirm the end-goal and priorities before a plan was established. The goal was to sell quickly for the highest price, but remain in the property for an extra month or so to finish a work commitment.

ProposedPlan

In my role of sharing information to help my client make informed decisions, I told her that optimal presentation and attractive pricing were both key success factors before creative and comprehensive marketing could begin. We toured the property together, and I compiled a list of key selling points, potential objections, and recommendations for how to get top dollar. We drafted a schedule together and got to work.

I connected my seller with an excellent local attorney upfront, because the antique home had numerous property easement changes on the deed over the years, so we could be proactive in sorting that out.

Conservative pricing

We reviewed the market data on both town-wide and neighborhood levels, and then looked at the closest comparable sales and potential competition for her property. We agreed to price conservatively to attract buyers and elicit enthusiasm versus critique when they came through. This also created competition for the home.

I invited a handful of agents from my office for a preview and endorsement of our price since there was very little immediate market data available to pinpoint a number.

Intentional home prep

Since curb appeal makes the first impression, we began there. A tree in front of the house was cute when she bought it three years earlier, but it since grew to hide the charming front porch and adorable covered terrace beneath, two key assets of the home. So it was important to the mission to remove it. The brick terrace had also been covered by a layer of green growth since it was last purchased.

So I connected her with my best landscaper to complete a full landscape refresh including tree removal, weeding, trimming, power-washing, and mulching.

The interior was well-maintained and had been updated by the prior owner, but it was packed full of large-scale furnishings from a prior residence that was more than three times the size. Most of the furnishings were cherished finds from chic furniture stores or specialty antique shops. So we focused on what had the biggest impact. We relocated some chairs to open the space and showcase the fireplace. We moved smaller pieces from window sills into storage to capitalize on the beautiful views of the gardens. And we identified other pieces that could be stored in the garage or sold.

That’s when I shared my estate sale contacts who helped to sell several armoires and an extra bed.

We used staging as a key marketing strategy to showcase the home’s assets and best use of space, streamline the focal points, and make a powerful emotional impression for buyers starting with the first glance at the curb.

Strategic timing& comprehensive marketing

It was going to take a few weeks to get the home ready amidst my client’s work and family obligations, but once the paperwork was complete, I began a marketing campaign to promote the Southport Village neighborhood where the house was located. This included a series of blog posts about the history and amenities of Southport Village that were shared across multiple social media channels.

Southport Village Video Shoot

Because the location was as much of an asset as the house itself, we filmed clips all over town, which also drew attention and conversation about the upcoming sale among passers by.

Once the house preparation was complete, I brought in my professional photography, video, drone, and floor plan crew.

The rollout capitalized on an in-office announcement just before the listing approached the market, use of the Coming Soon status in the Multiple Listing Service, and a yard sign with my agent rider to build momentum and pre-fill the upcoming showing schedule. This was followed by activating the listing for showings along with a full promotion on all websites and social channels to announce the new listing, broker tour, and the weekend of open houses.

I shared the new listing launch with my vast network via text thread, networking groups, social media groups, and email contacts.

The beautiful professional images and video were shared across dozens of websites and social media channels, email, and printed brochures, so that news could reach everyone wherever they were and whenever they were looking, 24/7.

Potential roadblock

My client had replaced the cedar roof on the detached garage with a licensed contractor but without obtaining a permit. Our buyer insisted that the seller obtain the permit before closing. The added layer was that the house was in the Southport Historic District and a flood zone, so those two departments needed to sign off in addition to the building and zoning departments in order to close the permit.

I connected my client with the Fairfield zoning department and historic commission to begin the permitting process. Ultimately, I also had to press them to come out for the final inspection in time for the closing!

Resources provided

Landscapers, staging insights, estate planners, photographers, videographers, drone specialists, the right attorney, town officials, office colleagues, and my vast network were key resources I provided to my client as we worked together to implement the plan.

This network, along with the countless technology platforms, digital subscriptions, and APPs I employ, helped to pull it all together.

The result

Several showings were pre-scheduled for the first few days of the active listing. The broker tour and two open houses had a non-stop flow of interested agents and potential buyers. We received an offer well-above the list price right away. We knew we could not keep that buyer waiting but wanted to honor the previously scheduled showings and open houses. So we made an offer deadline of noon on Monday, and by then, we had three offers to review. We reviewed the benefits and risks of each offer, accepted one, and sold the house for 17% above the asking price with a rent-back to my client at an agreed-upon rate, for a month and a half.

May 2026 photo collage with spring flowers and optimism!

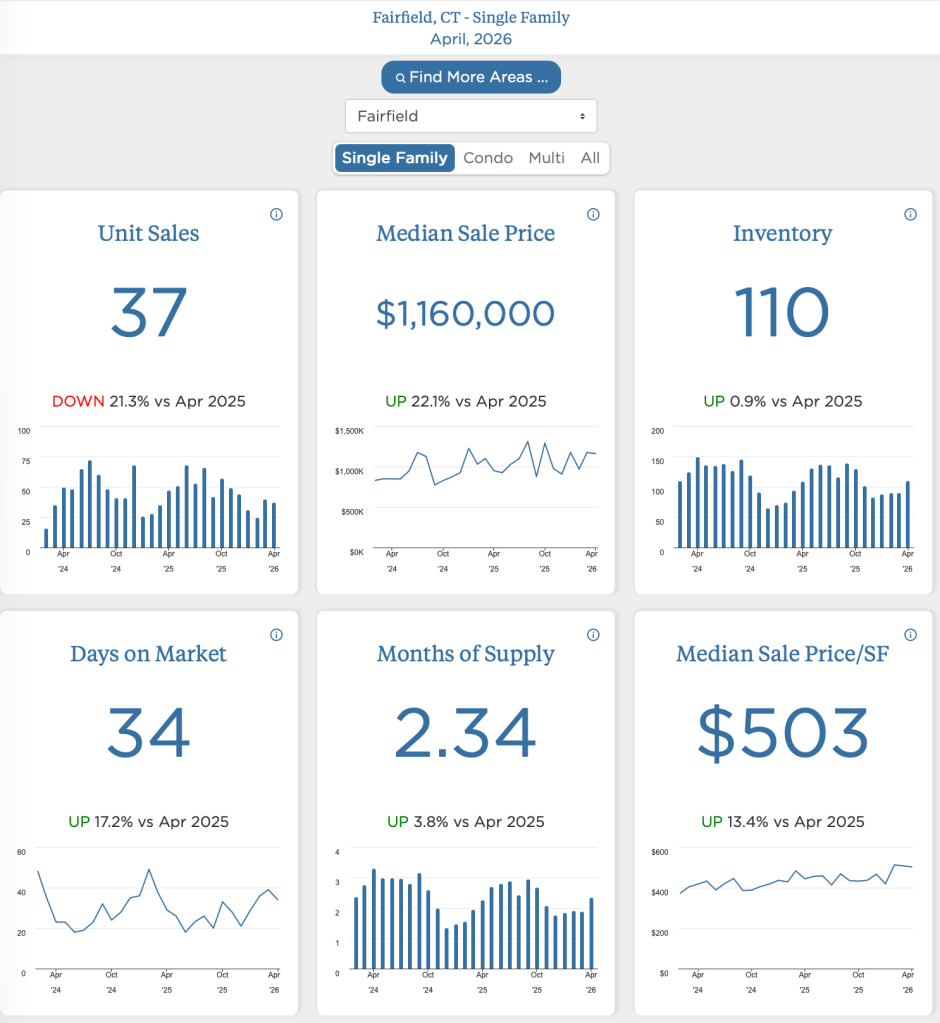

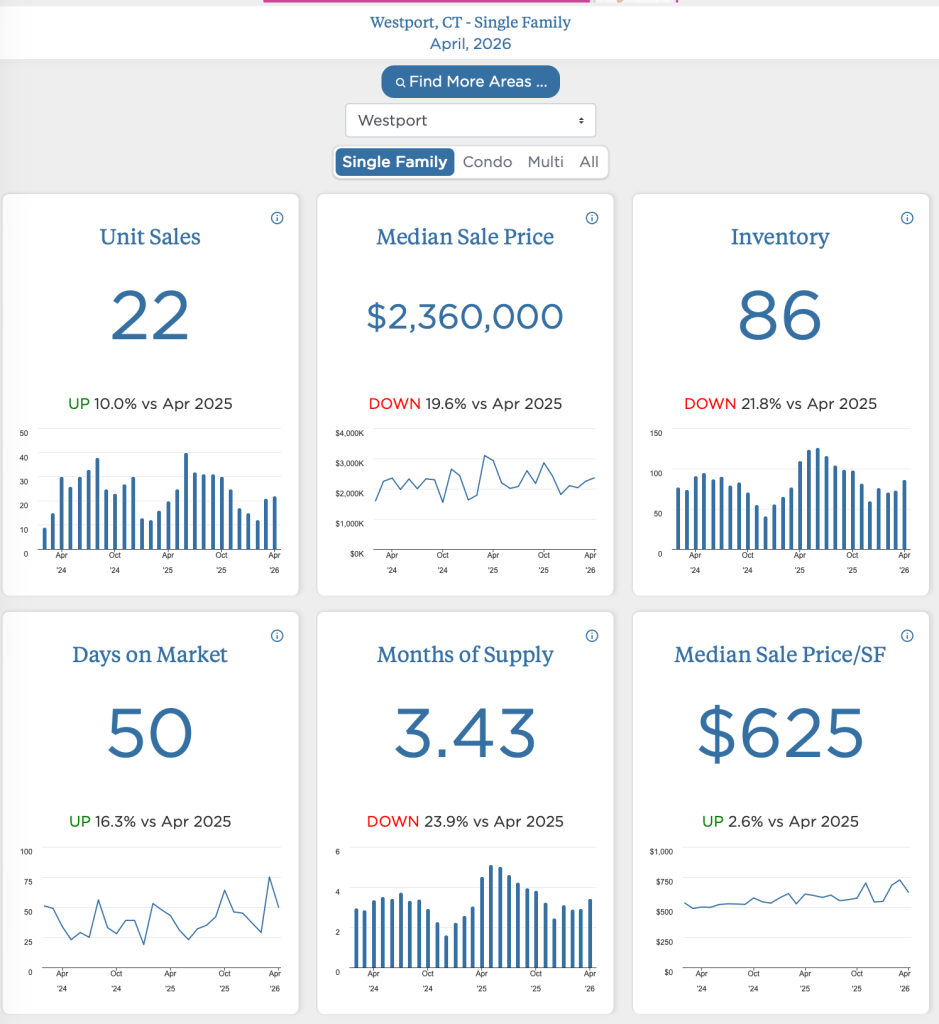

It’s May! 🌷 Here’s a summary of the Fairfield and Westport CT single-family markets in April 2026 compared to a year ago.

April 2026 Takeaways 📝

Low inventory continues, making it a competitive market for buyers, and giving sellers an advantage, in general.

On average, homes sold over the asking price, but this average reflects a wide variation.

There were a combination of bidding wars along with listings that sat on the market, and listings that reduced prices.

Buyers need to work with their agents to determine the market competition and other factors specific to the home they want to bid on to inform a strategic offer.

Sellers cannot take the low inventory situation for granted and must approach the market strategically as well in order to capitalize on buyer demand along with buyer fatigue.

As much as 42% of sales were cash deals.

In Fairfield, sluggish sales and increased inventory caused the housing supply to increase to 2.34 months-worth in April. These factors favored buyers, though prices were still up due to greater buyer demand than housing supply. Sellers signed contracts in an average of 34 days, though many accepted offers within a week. Other homes sat on the market and had price adjustments before securing an offer.

Homes sold for an average of 5% above the asking price. This reflected a wide range though, from 93% to 121% of the list price. Most homes sold close to full price, with 97% of homes selling at or above 95% of the list price. Cash deals accounted for 42% of the sales.

Unit sales were up in Westport, despite a 22% drop in inventory from the prior year bringing down the months of supply. The seller’s advantage continued. Days to contract averaged 50, which was an increase from the prior year.

Sale prices averaged 104% of asking. There was also a wide variation here, with a low of 93% up to as high as 122% of the price! Eighty-six percent of the sale prices were at or above 95% of the asking price. Thirty-two percent of the of the buyers in April reported using cash. A number of buyers withheld this information, so the percentage was likely higher.

What Are the Winning Strategies for Sellers and Buyers in Todays Local Markets?

Market Conditions in Fairfield and Westport Connecticut are characterized by continued low inventory, rising prices, some bidding wars, and some listings that are sitting and making price adjustments. There is some pent up demand from both buyers and sellers from a long harsh winter. Every home sale requires a strategy to suit personal goals and ideal positioning on the market.

Sellers, entering the market now still comes with the benefit of relatively low competition. But strategic pricing and optimal presentation are still critical for success.

You still need

✔️ Intentional home prep

Make sure to address obvious maintenance and repairs, both inside and out. Even though buyers may have to compete for a home in this market, they are still wary of maintenance and repair costs.

The exterior of your home makes the first impression regarding how much perceived deferred maintenance might be lurking inside.

Staging is a marketing strategy you can employ to showcase your home’s assets, show the best use of space, streamline the focal points, and make a powerful emotional impression that can seal your deal.

✔️ Conservative pricing

Pricing conservatively will attract buyers to generate competition for your listing. Doing so will also create enthusiasm versuscritique when they walk through.

✔️ Strategic timing

Ask your agent what the rollout plan is and why.

✔️ Aggressive marketing

Ask your agent for your custom marketing plan and schedule.

How can you coordinate a purchase with your home sale?

If you are looking to buy and worry about coordinating your sale with finding your new home, you can protect yourself in the transition when you list your house “subject to finding suitable housing”. This means you are under no obligation to sell your house until you have found the new home.

Another option is to sell your house and rent it back until you’re ready to move. This puts cash in your pocket and positions you as a strong buyer.

You can also request a long closing to give you time to find and close on your new home.

Consider using a Pod for storage and planning to get an AirBnB to ease your transition. This way you are already partially packed for your move and can take your time to decide on where you want to be without trying to match up any timelines.

You can opt for a short term bridge loan for your purchase that you pay back when you sell your house.

Talk to your agent and mortgage broker about a strategy that works best for you. Putting your house on the market enables you to be a competitive buyer while expanding the housing choices for everyone out there shopping for a home!

Buyers, you may face multiple offers or have leverage to negotiate depending on the competition for the home of interest. It’s critical to have your budget set, down payment saved, and credit score in good order. Remember to avoid applying for financing of additional large purchases before and during a mortgage application process!

If you see something you like, be prepared to have your agent submit a complete and competitive offer including your pre-approval or proof of funds. If you need to sell your house first, talk to your agent as soon as possible to determine your strategy.

Keep in mind that you will likely be competing with cash offers, which are very attractive to sellers. Cash comes deals are much simpler and with less risk: no appraisal, no interest rate variables, no credit or job stability requirements.

So if you are financing, it’s important to do everything possible to make your offer attractive compared to the ease of cash.

Contact your agent to help you plan for your new home this year.

Fairfield and Westport CT single-family markets in February 2026 compared to 2025.

February sales were lack-luster compared to the same time in 2025, likely due to the frigid temperatures and ample snow in January. However, as ‘winter’ headed toward the rearview mirror, more sellers began to enter the market causing a rise in inventory. Competition among buyers remained stiff with many homes selling above the list price.

Contact your agent to help you plan for your new home this Spring! 🏡 🌱☀️

More Action Items

Secure regular updates: new listings, price changes, local market insights, and mortgage rates.

Photo collage depicting spring onset with the welcome warmth of the sun!

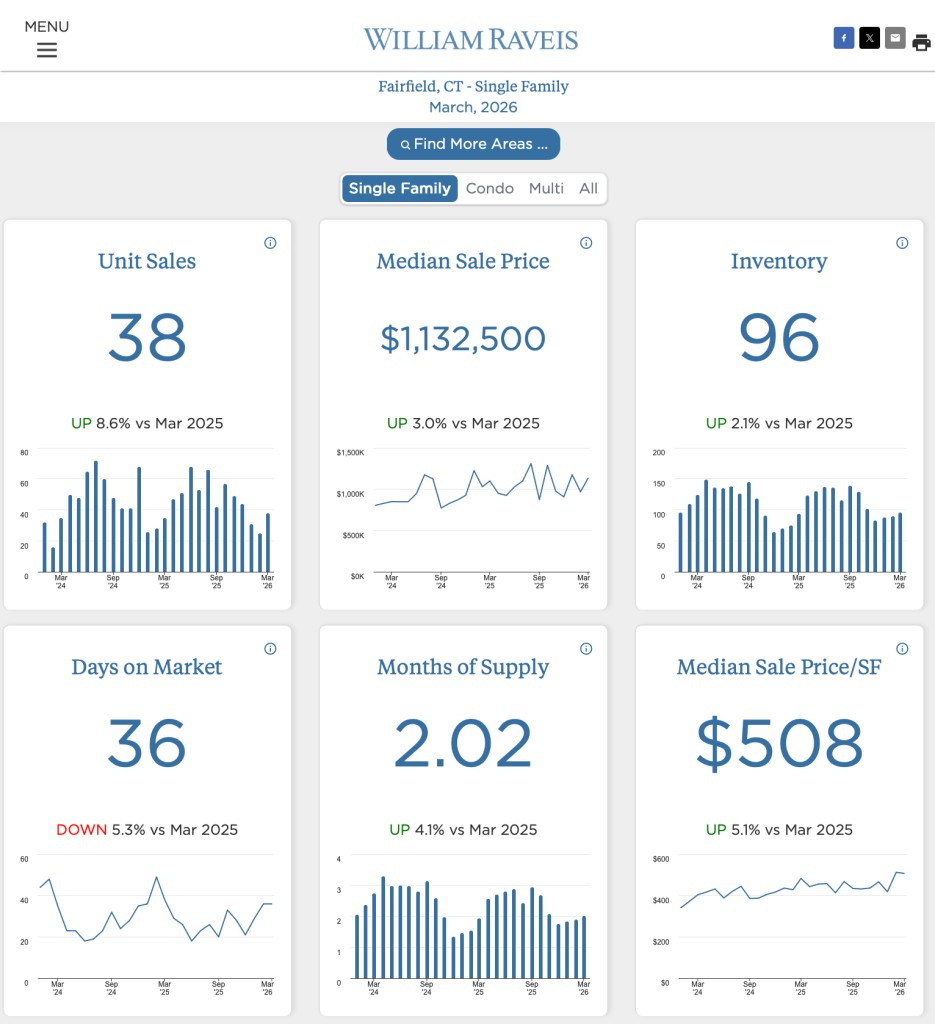

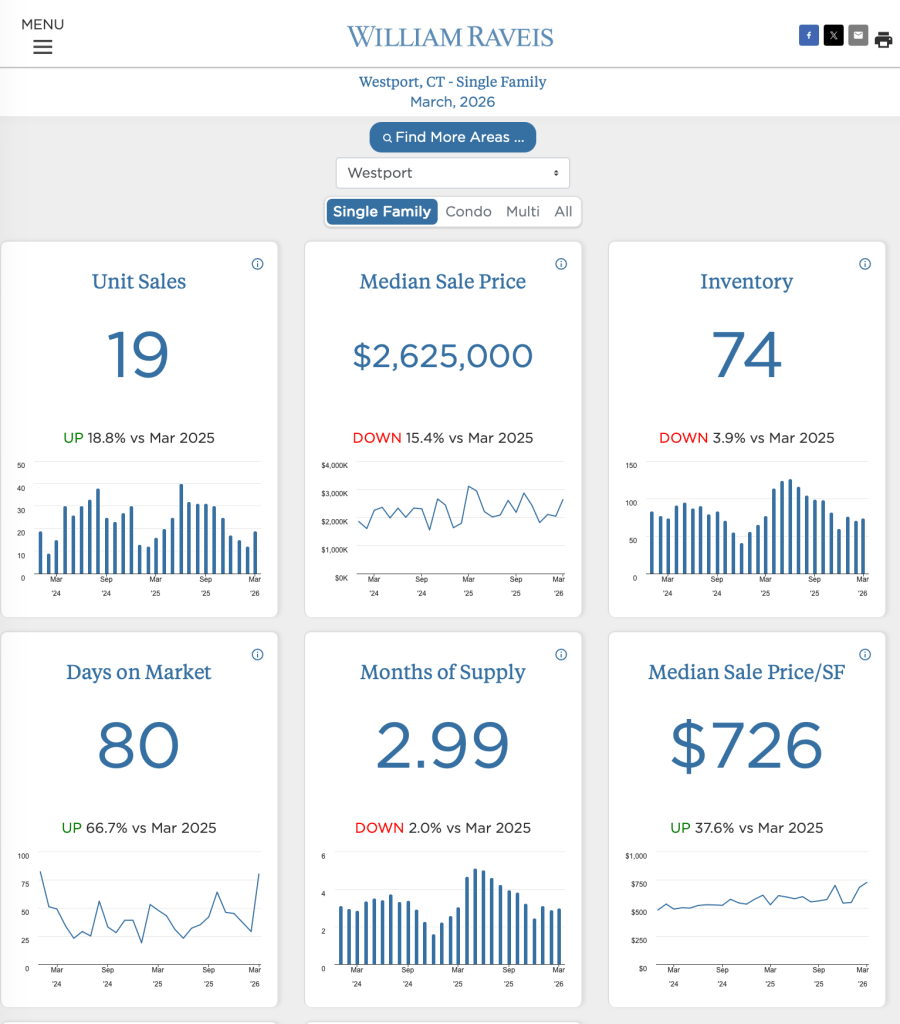

Welcome Spring! 🌱 Here’s a summary of the Fairfield and Westport CT single-family markets in March 2026 compared to a year ago.

March2026 Takeaways 📝

In Fairfield, the sellers’ market continued, with just 96 single-family homes for sale and two months of supply despite a small increase in inventory from the prior year. The average time on market was a little over a month to contract. The median sale price and price per square foot was also higher than a year ago. Sales activity was up nearly 9% from March 2025, suggesting that more people are ready to get into the market and commit to their lifestyle goals.

Homes sold for an average of 4% above the asking price. This reflects a wide range though, from 83% to 124% of the asking price. Most homes sold close to full price, with just 13% of sales below 95% of the list price. Cash deals accounted for 37% of the sales.

Unit sales were also up In Westport, despite a dip in inventory from the prior year. The seller’s advantage continued here as well. Housing inventory was down 4% from the previous year with 74 houses for sale, and there were just under three months worth of supply. Days on market averaged 80, a nearly 67% increase over the prior year.

Sale prices averaged 102% of asking. There was also a wide variation here, with a low of 78% of the list price up to as much as 134% of the price! Interestingly though, 26% of the sale prices were under 95% of the asking price. So this average is made of extremes, and each sale is unique depending on the demand and perceived value for that particular property at the time it hits the market. A significant 62% of the sales in March were made with cash!

Sales Were Up

Sales activity was up in both towns compared to a year ago. Inventory was still low but appeared to be starting to trend upward. The spring market was delayed by extreme winter weather conditions this year, but more homes were beginning to arrive on the market.

The Opportunities… ✅

Rates areholding steady with the 30-year fixed conforming mortgage rateat 6.125% and the jumbo rate at 6.000% at the time this was written. William Raveis Mortgage also offers adjustable rate mortgages (ARMs) with rates in the low-five percent range.

Sellers, if you enter the market now, you still benefit from low competition.

Concerned about coordinating a purchase with your home sale?

If you are looking to buy and worry about coordinating your sale with finding your new home, you can protect yourself in the transition when you list your house “subject to finding suitable housing”. This means you are under no obligation to sell your house until you have found the new home.

Another option is to sell your house and rent it back until you’re ready to move. This puts cash in your pocket and positions you as a strong buyer.

You can also request a long closing to give you time to find and close on your new home.

You can opt for a short term bridge loan for your purchase that you pay back when you sell your house.

Talk to your agent and mortgage broker about a strategy that works best for you. Putting your house on the market enables you to be a competitive buyer while expanding the housing choices for everyone out there shopping for a home!

Buyers, depending on the competition for the home you are bidding on, you may face multiple offers or you could have leverage to negotiate. Remember to have your budget set, down payment saved, and credit score in good order. Avoid taking out other loans or financing other large purchases before and during a mortgage application process! If you see something you like, be prepared to have your agent submit a complete and competitive offer including your pre-approval or proof of funds. If you need to sell your house first, talk to your agent as soon as possible to determine your strategy.

Contact your agent to help you plan for your new home this year! 🏡 🌱☀️

More Action Items

Secure regular updates: new listings, price changes, local market insights, and mortgage rates.

There are certain details in Southport Village that you don’t notice at first.

They don’t announce themselves like the harbor views or the stately 19th-century homes. They aren’t framed in listing photos or highlighted in brochures.

And yet—they may be one of the most authentic, enduring elements of the village.

Look down.

Along the edges of the quiet lanes, bordering gardens and gravel drives, you’ll find them: …not flashy new countertops, but granite curbs, worn softly by time.

The Beauty Beneath Your Feet

Long before asphalt roads and modern infrastructure, New England villages relied on hand-hewn granite to define their streets.

In Southport, many of these stones still remain.

Cut from regional quarries in the 18th and 19th centuries

Split by hand or early tools, not machines

Set in place to manage drainage, define carriage paths, and bring order to growing coastal communities

Over time, they’ve taken on a quiet elegance:

Edges softened by decades of footsteps and carriage wheels

Subtle variations in tone—silver, ash, and salt-washed gray

Imperfections that feel less like flaws and more like fingerprints of history

These are not just curbs. They are artifacts woven into daily life.

A Living Streetscape

One of the defining characteristics of Southport Village is its continuity—a rare sense that the past hasn’t been replaced, only gently adapted.

Even when roads are improved or utilities updated, the granite curbing is often:

Carefully lifted

Preserved

And reset in place

This means that what you see today is often a blend of:

Original 19th-century stone

Reclaimed historic granite

Thoughtful stewardship by the community

The result is a streetscape that feels timeless rather than restored.

A Closer Look at 494 Pequot Court

At 494 Pequot Court, this story continues in a particularly compelling way.

Set within a quiet enclave just off Pequot Avenue, the property reflects the same layered history found throughout the village—where every detail, even at ground level, contributes to a sense of place.

Along the edge of the property, the granite curbing reveals:

A natural split-face texture, characteristic of traditional quarrying methods

Subtle weathering, suggesting age and exposure

A clean, intentional alignment, indicating it has likely been carefully reset over time

This combination is especially appealing.

It offers:

The authentic materiality of historic Southport

With the stability and refinement of more recent stewardship

In other words, it’s not just original—it’s enduring.

Why These Details Matter to Buyers

For those drawn to Southport Village, the appeal is rarely about square footage alone.

It’s about:

Texture

Atmosphere

Authenticity

Granite curbing may seem like a small detail, but it signals something much larger:

✔ A commitment to preserving historic character ✔ A neighborhood that values continuity over convenience ✔ A setting where even infrastructure reflects craftsmanship

For buyers seeking more than just a home—for those looking for a sense of place—these details resonate.

The Quiet Luxury of Authenticity

In today’s world, where so much is newly built to look old, Southport offers something different:

The real thing.

Not replicated. Not manufactured. But lived-in, weathered, and quietly beautiful.

And sometimes, the most compelling evidence of that isn’t in the architecture above—

—but in the stone beneath your feet.

Explore More

If you’re exploring Southport Village real estate or are curious about the history and hidden details that make this coastal enclave so special, stay tuned for more posts in this series, or consider venturing over to the vibrant Fairfield Beach Area.

Or, if you’d like a private look at 494 Pequot Court, I’d be happy to share more about the home—and the story it continues to tell.

Because in Southport, even the smallest details are part of something much bigger.

Charming Pied-a-Terre in Connecticut’s Alluring Southport Village! Whether you’re looking for a permanent residence or your home away from home, welcome to the perfect vacation home or condo alternative. Leave without a care or immerse yourself in this historic maritime enclave. A rare find in the heart of the Village, this home is steps from eateries, shops, metro, pub, bakery, post office, the Equinox, Southport Harbor, and Southport Beach. -All an hour from NYC!

The covered front porch welcomes you and the enchanting rear stone terrace among lush gardens offers the ultimate private retreat. Inside, elegant interiors unfold. An inviting Living Room with hardwood floors, hidden TV, and a gas fireplace opens to the Dining Area. The renovated Chef’s Kitchen features a Caesarstone island, stainless appliances, and a light-filled eating area with built-ins and a banquette overlooking the garden. Upstairs is a serene Primary Suite and stunning spa bath, hardwood floors, and 9-foot ceiling. A Guest Bedroom, hall bath, laundry, and access to Attic Storage complete the second floor.

The Walkout Lower Level offers a versatile Home Office or Family Room with a cozy gas fireplace. It connects to a crafting area with a porcelain sink, storage, and a separate entrance to the quaint private terrace, offering guest-suite potential. Enjoy the perfect blend of character, privacy, and convenience in one of Connecticut’s most treasured seaside villages.

Renovated kitchen and baths, new cedar roof on the garage, new oil & stone driveway, new microwave with boost exhaust, new drinking water filter in kitchen, renewed gas fireplace in the lower level, and a full landscape refresh.

Whole-house generator, in-ground irrigation and garden pot-filler, Thermopane windows, and lower-level fireplace with heat blower.

Convenient second-floor laundry with an additional hook-up in the lower level. Central air, (on main two floors), auto lighting on exterior and inside closets, 200 AMP electrical service with underground cables, city water and sewer. Private road with granite curbstones.

If you would like more information about this home or would like to discuss your plans, please submit a request below.

I pulled up my own credit report on camera and walked through every factor live 😅. Here’s exactly what goes into your score — and why each one matters when you’re buying or selling a home.

Your credit score is calculated using five specific factors, each weighted differently. Understanding the breakdown doesn’t just satisfy curiosity — it gives you a roadmap to improve your score strategically before you enter the real estate market.

Below is the exact framework the major credit bureaus use, paired with what it means for home buyers and sellers here in Fairfield County.

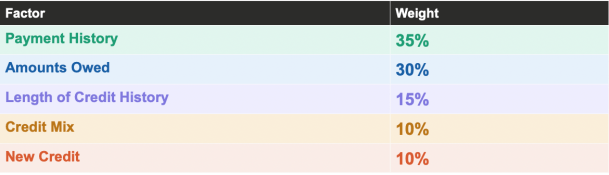

This is the most heavily weighted element in your score for good reason: lenders want to know, above everything else, whether you pay your bills on time. Every on-time payment builds your score. Every missed or late payment damages it — and that damage lingers on your report for up to seven years. Even one 30-day late payment can drop a good score by 60–110 points.

🏡 Realtor Tip: If you’re planning to buy in Fairfield County in the next 6–12 months, set every account to autopay minimum payments today. One forgotten bill can cost you thousands in mortgage interest.

FACTOR 2 · 30% OF YOUR SCORE

Amounts Owed — Your credit utilization ratio

This factor measures how much of your available revolving credit you’re currently using. It’s expressed as a percentage — if you have a $10,000 credit limit and carry a $3,000 balance, your utilization is 30%. Lenders want to see this number below 30%, and ideally below 10% for the strongest scores. Maxed-out cards are a major red flag, even if you pay them off monthly.

🏡 Realtor Tip: Paying down balances before applying for a mortgage is one of the fastest ways to boost your score. Unlike late payments, utilization improvements can show up on your report within 30 days of paying down a balance.

FACTOR 3 · 15% OF YOUR SCORE

Length of Credit History — Time is on your side

The longer your credit accounts have been open and active, the better. This factor considers the age of your oldest account, your newest account, and the average age of all accounts. This is why financial advisors often caution against closing old credit cards — even ones you no longer use. Closing an old account shortens your average credit age and can ding your score.

🏡 Realtor Tip: Don’t close unused credit cards in the months before buying a home. Keep them open with a small recurring charge (like a streaming subscription) paid automatically each month.

FACTOR 4 · 10% OF YOUR SCORE

Credit Mix — Variety shows responsibility

Lenders like to see that you can manage different types of credit responsibly. A healthy mix includes revolving credit (credit cards), installment loans (auto, student, personal), and ideally a mortgage. You don’t need one of every type — and you should never open new accounts just to diversify. But if you only have credit cards, adding a small installment loan over time can gradually help your mix.

🏡 Realtor Tip: This factor matters least in the short term. Don’t make major financial decisions — like taking out a new loan — just to improve your credit mix before buying a home.

FACTOR 5 · 10% OF YOUR SCORE

New Credit — Every application leaves a footprint

Each time you apply for new credit, the lender performs a “hard inquiry” on your report. One inquiry typically costs you 5–10 points and stays on your report for two years. Multiple applications in a short window — outside of rate shopping for a single mortgage — can signal financial stress to lenders. The good news: mortgage-related inquiries within a 45-day window are typically grouped and counted as just one.

🏡 Realtor Tip: Avoid opening any new credit accounts — cards, car loans, store financing — in the 6 months before applying for a mortgage. Even a single new account can raise lender questions at underwriting.

Frequently Asked Questions

How often is my credit score updated?

Your credit score updates whenever your lenders report new information to the bureaus — typically once a month. This means improvements from paying down balances or making on-time payments can show up relatively quickly, usually within 30–60 days.

Which credit score do mortgage lenders use?

Most mortgage lenders use FICO scores — specifically FICO 2, FICO 4, and FICO 5 — pulled from all three major bureaus (Equifax, Experian, and TransUnion). They typically use the middle of the three scores. This may differ from the score you see on free monitoring apps, which often use VantageScore.

How much can I realistically improve my score before buying?

It depends on what’s holding your score down. Paying off high balances can produce significant improvement in 30–60 days. Clearing up errors through a dispute can take 30–45 days. Recovering from a late payment or collection takes longer — typically 12–24 months of clean history. Most buyers can meaningfully improve their score in 3–6 months of focused effort.

Should I check my own credit report before talking to a lender?

Absolutely — and you should do it at least 3–6 months before you plan to buy. This gives you time to dispute errors, pay down balances, and address any surprises before a lender sees your file. You can access your free report from all three bureaus at AnnualCreditReport.com.

Want to know where your credit stands before buying in Fairfield, Southport, Westport and beyond? I work alongside William Raveis Mortgage to help buyers understand their credit picture before they ever start touring homes. Reach out and let’s talk about getting you — and your score — ready to compete.