June is here! 🌞 Here’s a summary of the Fairfield and Westport CT single-family markets in May 2026 compared to a year ago.

May 2026 Takeaways 📝

- Inventory was still low but was rising.

- On average, homes sold 3-5% over the asking price, but this average reflects a wide range.

- Some homes sold way over asking with bidding wars and others sat on the market, or had price reductions.

- Market time was up in both towns.

- Buyers need to work with their agents to determine the best way to approach an offer based on the conditions specific to the home of interest, since competition is case-by-case.

- Sellers must approach the market strategically to capitalize on buyer demand balanced with buyer fatigue and be perceived as the best value available for the price.

- If you are financing, your offer needs to be extra attractive because you may be competing with cash offers that are very attractive to sellers due to their simplicity. As much as 46% of the May sales were cash deals in Westport, and 28% in Fairfield.

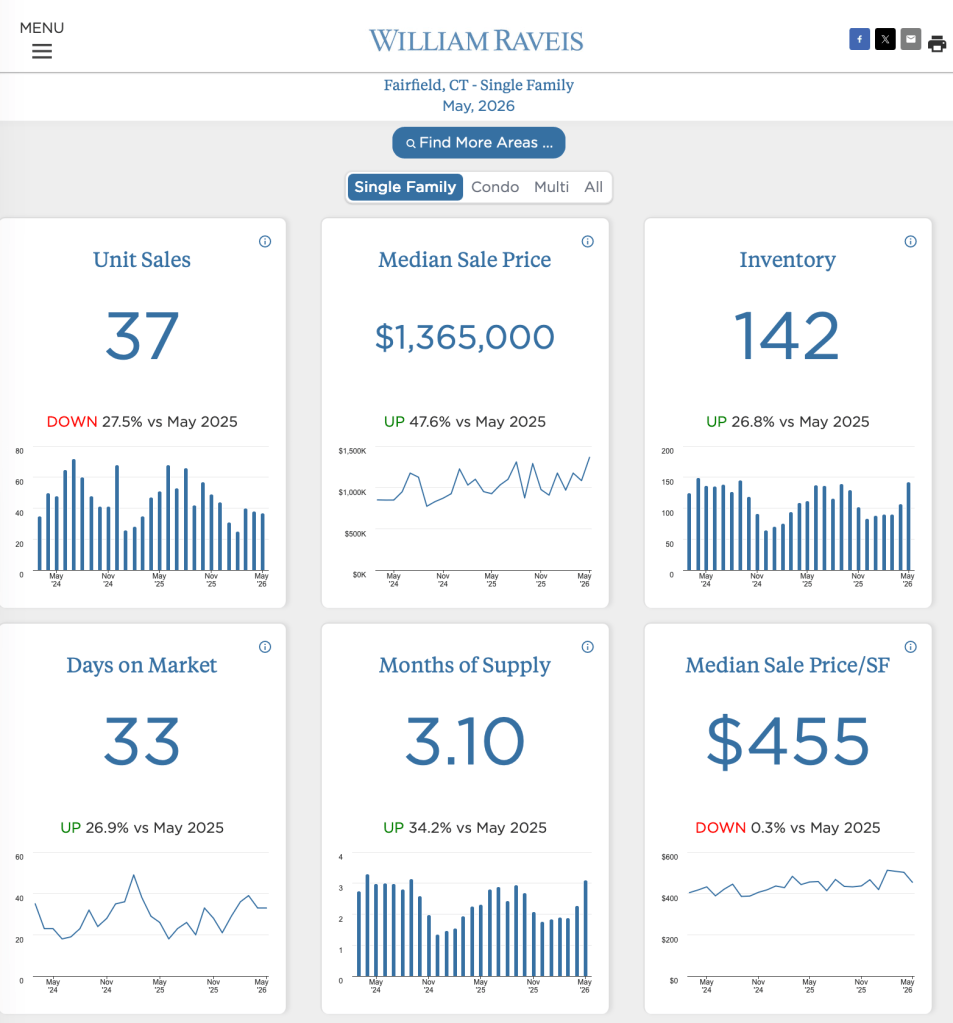

In Fairfield, sales were down 28% from last year, while inventory was 27% higher. The housing supply increased to 3.1 months-worth in May. These factors were helpful for buyers, though the median sale price was way up, 48%, compared to last May. Market time was longer than last May with an average of 33 days to contract, and 11% of homes took 90 days or more to get a signed contract.

Homes sold for an average of 105% of the asking price. This reflected a huge range though, from 79% to 138% of the list price! Most homes sold close to full price, with 86% of homes selling at or above 95% of the list price. Cash deals accounted for 28% of the sales, significantly fewer than last month.

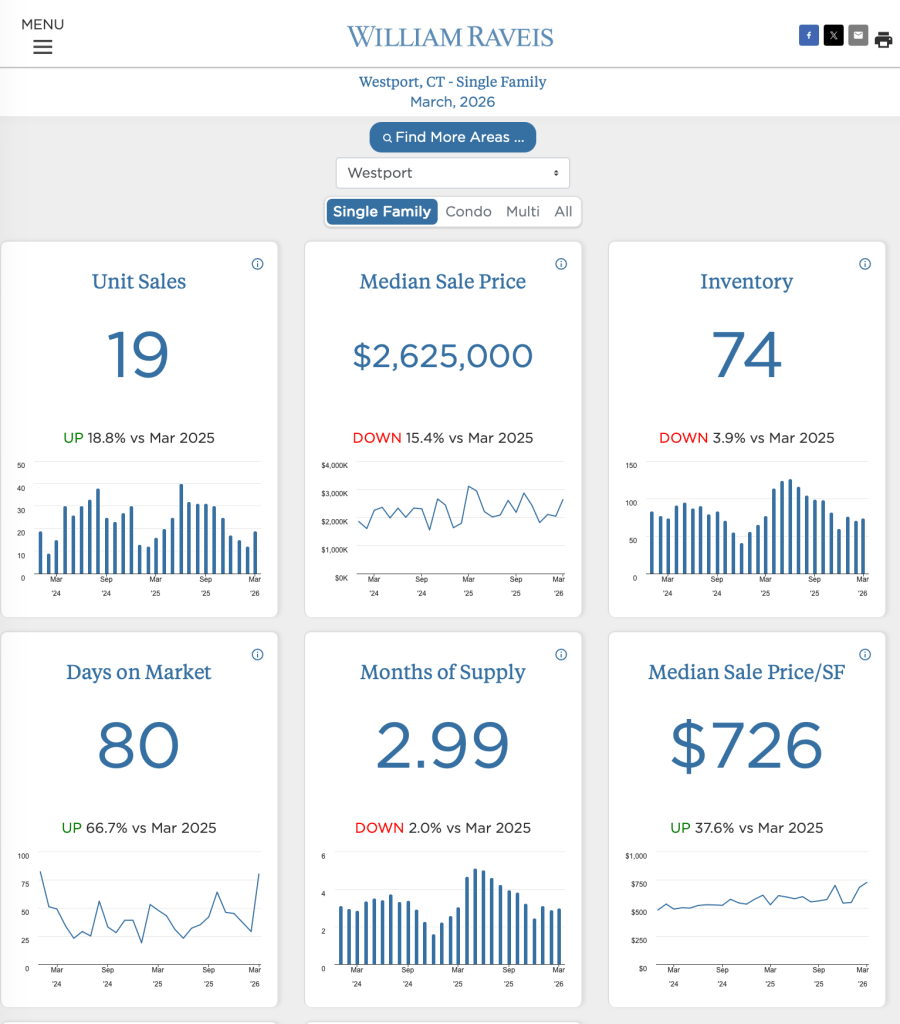

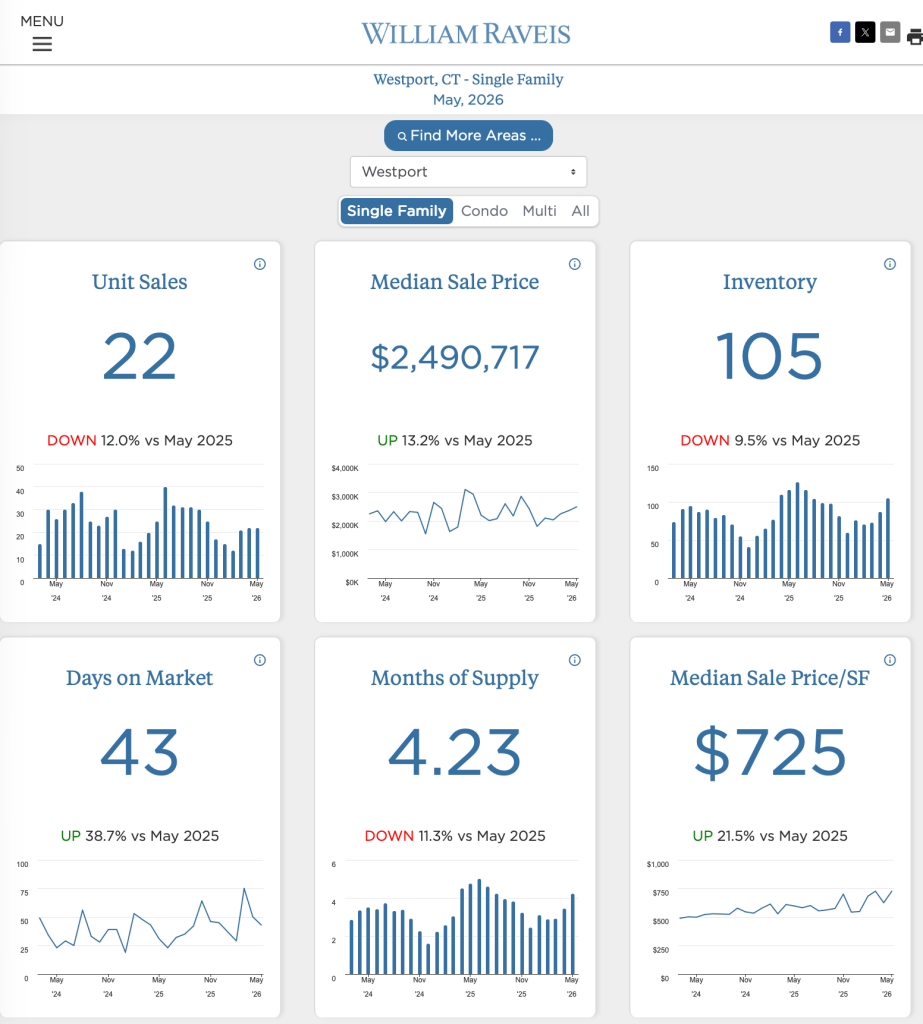

Sales and inventory were down in Westport, compared to May 2025. The months of supply metric was also down to 4.23 months, though this reflected an increase from last month. Days to contract averaged 43, which was a significant increase from the prior year, though fewer than last month.

Sale prices averaged 103% of asking. There was also a wide variation here, with a low of 94% up to as high as 121% of the price. Ninety-one percent of the sale prices were at or above 95% of the asking price. Forty-six percent of the of the buyers in May reported using cash. A number of buyers withheld this information, so the percentage could be higher.

Spring 2026 Fairfield & Westport Real Estate Market: Trends, Pricing & Winning Strategies ✅

More Action Items

- Get monthly updates for your zip code: new listings, price changes, local market insights.

- See last month’s market report.

- Track your home’s current value.

- Request LIVE Trend Reports for your town.

- Share 10 Reasons to Come to Fairfield with a friend!

- Request the Quarterly Beach Bulletin 🌊 in your mailbox below (include your mailing address).

#MarketReport

#RealEstateMarket

#FairfieldCTRealEstate

#WestportCTRealEstate

#HomeBuyers

#HomeSellers

#LuxuryLifestyle

#LuxuryRealEstate

#WilliamRaveisRealEstate

#WilliamRaveis

#RaveisSouthport

#DreamHome

#HomeSweetHome

#MyHomeIsMyCastle

#RealEstateMarket

#HousingPredictions

#MortgageRates