Is it better to buy now or buy later?

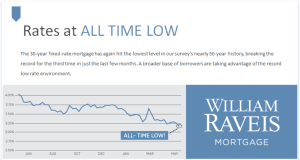

This is always a dilemma for home buyers and would-be sellers. The biggest question on everyone’s mind at the time of this post is where are interest rates going?

According to global economist, Dr. Marci Rossell in a webinar on December 6th from Leading Real Estate Companies of the World, rates are likely to be stuck in a holding pattern in the six percent range until as late as April or May next year. She said we won’t know where rates will be going until we see what happens with tariffs and deportation, which will impact labor and prices.

Regardless of what the future holds, it is not recommended to bank on interest rate predictions, because the reality is that nobody really knows for sure what will happen. This summer, the assumption was that rates were coming down by the end of the year and through 2025, however, this was not the case.

What if you could run some scenarios with various assumptions and see which outcomes look most favorable for you? I have an excellent tool that can do just that!

Should I buy it now or wait a couple years when interest rates may be lower, and how does appreciation figure in to it?

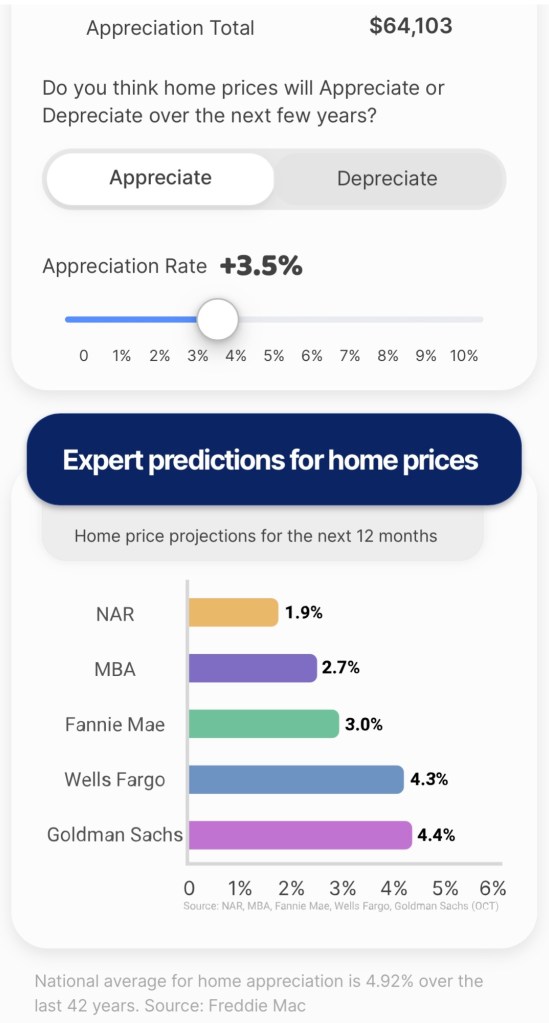

Several economic authorities estimate that real estate values will continue to rise by an average of 3.5% in the next year. This means that homeowner equity will grow. But what if rates are lower in another year or two?

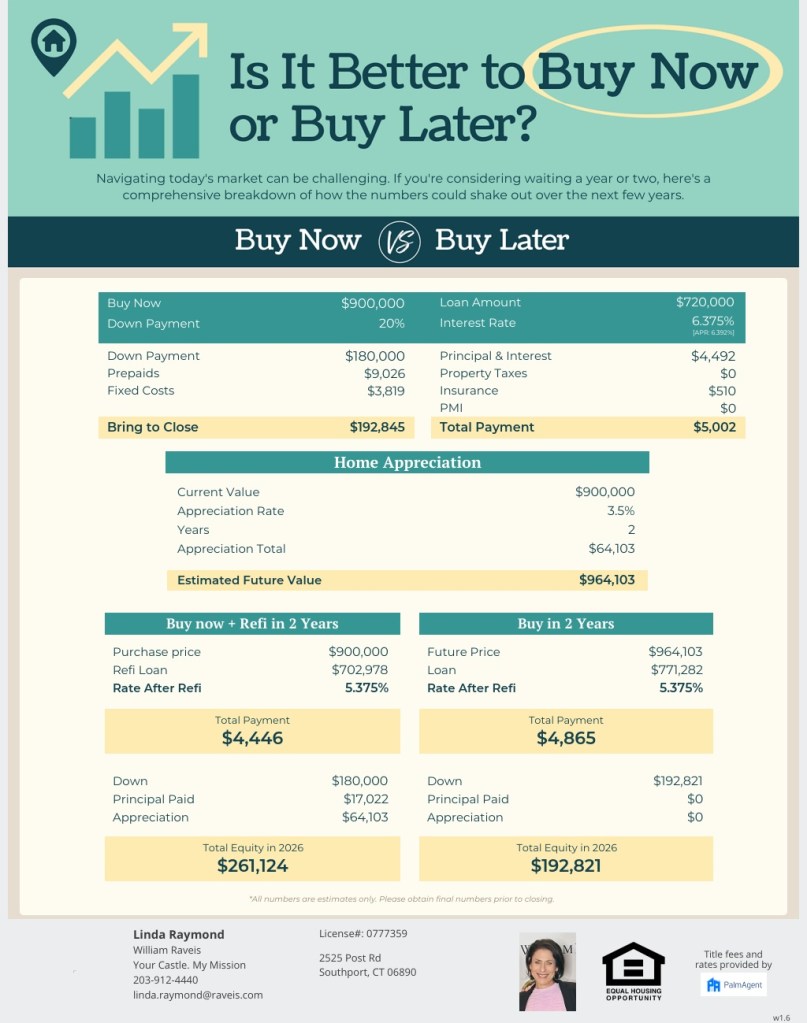

Take a look at the report from my calculator. The example shows a $900,000 home purchase today with 20% down and an interest rate of 6.375% with refinancing in two years to a potential lower interest rate of 5.375%. The calculator compares this approach to waiting two years and purchasing the same home at the lower rate.

Buying now results in a monthly payment of $4,446 and $261,124 in equity after two years, when then you can refinance. After waiting two years, the purchase price is approximately 3.5% higher due to appreciation, resulting in a purchase price of $964,103. The loan for this house may be at a lower rate, but it is now a bigger loan resulting in payments of $414 more each month. Also, this new homeowner has $68,303 less equity than if they had bought the house two years earlier.

If the rates didn’t change, buying later would result in even higher monthly payments due to the larger loan at the higher rate. In this example, purchasing today, would have achieved a lower price, smaller loan, lower monthly payments, and more equity.

I’m happy to calculate different scenarios with varied assumptions for you. Do you think home values will go up or down? What do you think rates will be in two years? What is your home buying budget? What is your dream lifestyle! Reach out to me, and let’s run some scenarios and talk about your plans!

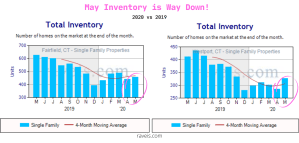

Look at the difference in the number of homes for sale in Fairfield and Westport in May compared to May of 2019! The marketplace is in need of more homes for sale. This creates a huge opportunity for sellers!

Look at the difference in the number of homes for sale in Fairfield and Westport in May compared to May of 2019! The marketplace is in need of more homes for sale. This creates a huge opportunity for sellers!

The real estate marketplace is very busy right now for a few key reasons. Realtors and everyone else in the industry have adapted to working in safe mode, there is pent up demand from the initial pandemic slowdown, and

The real estate marketplace is very busy right now for a few key reasons. Realtors and everyone else in the industry have adapted to working in safe mode, there is pent up demand from the initial pandemic slowdown, and

Your Realtor may have worked patiently and tirelessly to successfully negotiate optimal terms for you thus far only to then work triple-time behind the scenes to keep your purchase or sale together because the attorneys are butting heads. You may know nothing about this unless your sale falls through because of it. You want to work with a lawyer that relates professionally with all parties in the transaction at all times. Otherwise, they are being counter-productive and are doing you (and everyone else involved) a disservice.

Your Realtor may have worked patiently and tirelessly to successfully negotiate optimal terms for you thus far only to then work triple-time behind the scenes to keep your purchase or sale together because the attorneys are butting heads. You may know nothing about this unless your sale falls through because of it. You want to work with a lawyer that relates professionally with all parties in the transaction at all times. Otherwise, they are being counter-productive and are doing you (and everyone else involved) a disservice.

If any of the players are “missing in action” it prevents the process from progressing efficiently, and critical information can fall through the cracks.

If any of the players are “missing in action” it prevents the process from progressing efficiently, and critical information can fall through the cracks.

Ask any lender or real estate agent what’s important about an attorney, and they will tell you efficiency (second to good communication)! The entire transaction is on the clock from the moment an offer is accepted. The attorney must send and receive the contract in the allotted timeframe and then get it to the lender. They must complete a title search and address questions and concerns in a timely fashion, and they need to prepare all the closing documents on time, or your closing could be postponed.

Ask any lender or real estate agent what’s important about an attorney, and they will tell you efficiency (second to good communication)! The entire transaction is on the clock from the moment an offer is accepted. The attorney must send and receive the contract in the allotted timeframe and then get it to the lender. They must complete a title search and address questions and concerns in a timely fashion, and they need to prepare all the closing documents on time, or your closing could be postponed. Many of the questions above are not ones you can easily get answers to by interviewing the attorney directly or even from a friend who’s used him or her. If your agent hasn’t worked with the lawyer directly, he or she can ask other agents how well that attorney as served his client and worked as a team player for a successful transaction in the past. Your agent’s only interest in the attorney you hire is to get a solid team member on board to help ensure a smooth move for you!

Many of the questions above are not ones you can easily get answers to by interviewing the attorney directly or even from a friend who’s used him or her. If your agent hasn’t worked with the lawyer directly, he or she can ask other agents how well that attorney as served his client and worked as a team player for a successful transaction in the past. Your agent’s only interest in the attorney you hire is to get a solid team member on board to help ensure a smooth move for you!

So more and more real estate websites and blogs are becoming mobile friendly and optimizing for the best mobile experience. Mobile apps are also on the rise. William Raveis provides a comprehensive

So more and more real estate websites and blogs are becoming mobile friendly and optimizing for the best mobile experience. Mobile apps are also on the rise. William Raveis provides a comprehensive