Is it better to buy now or buy later?

This is always a dilemma for home buyers and would-be sellers. The biggest question on everyone’s mind at the time of this post is where are interest rates going?

According to global economist, Dr. Marci Rossell in a webinar on December 6th from Leading Real Estate Companies of the World, rates are likely to be stuck in a holding pattern in the six percent range until as late as April or May next year. She said we won’t know where rates will be going until we see what happens with tariffs and deportation, which will impact labor and prices.

Regardless of what the future holds, it is not recommended to bank on interest rate predictions, because the reality is that nobody really knows for sure what will happen. This summer, the assumption was that rates were coming down by the end of the year and through 2025, however, this was not the case.

What if you could run some scenarios with various assumptions and see which outcomes look most favorable for you? I have an excellent tool that can do just that!

Should I buy it now or wait a couple years when interest rates may be lower, and how does appreciation figure in to it?

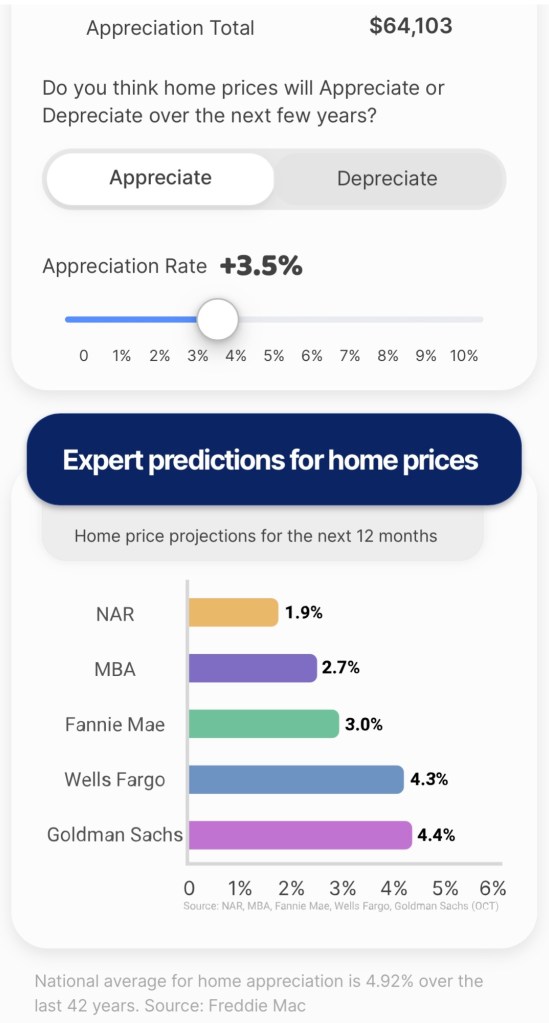

Several economic authorities estimate that real estate values will continue to rise by an average of 3.5% in the next year. This means that homeowner equity will grow. But what if rates are lower in another year or two?

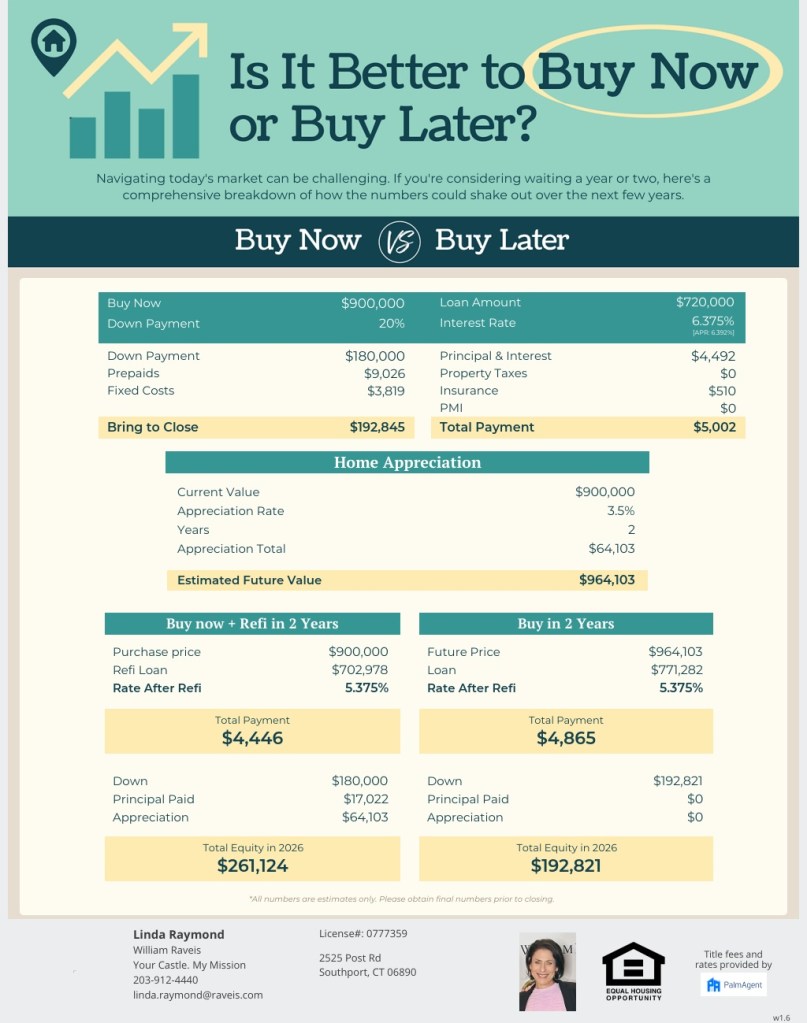

Take a look at the report from my calculator. The example shows a $900,000 home purchase today with 20% down and an interest rate of 6.375% with refinancing in two years to a potential lower interest rate of 5.375%. The calculator compares this approach to waiting two years and purchasing the same home at the lower rate.

Buying now results in a monthly payment of $4,446 and $261,124 in equity after two years, when then you can refinance. After waiting two years, the purchase price is approximately 3.5% higher due to appreciation, resulting in a purchase price of $964,103. The loan for this house may be at a lower rate, but it is now a bigger loan resulting in payments of $414 more each month. Also, this new homeowner has $68,303 less equity than if they had bought the house two years earlier.

If the rates didn’t change, buying later would result in even higher monthly payments due to the larger loan at the higher rate. In this example, purchasing today, would have achieved a lower price, smaller loan, lower monthly payments, and more equity.

I’m happy to calculate different scenarios with varied assumptions for you. Do you think home values will go up or down? What do you think rates will be in two years? What is your home buying budget? What is your dream lifestyle! Reach out to me, and let’s run some scenarios and talk about your plans!