FAIRFIELD COUNTY REAL ESTATE · CREDIT EDUCATION

I pulled up my own credit report on camera and walked through every factor live 😅. Here’s exactly what goes into your score — and why each one matters when you’re buying or selling a home.

Your credit score is calculated using five specific factors, each weighted differently. Understanding the breakdown doesn’t just satisfy curiosity — it gives you a roadmap to improve your score strategically before you enter the real estate market.

Below is the exact framework the major credit bureaus use, paired with what it means for home buyers and sellers here in Fairfield County.

(Text version for searchability:)

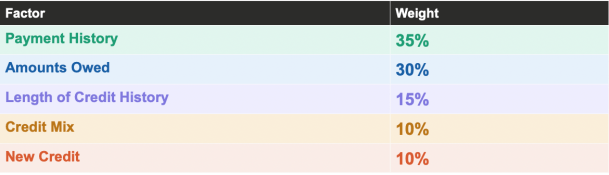

| Factor | Weight |

| Payment History | 35% |

| Amounts Owed | 30% |

| Length of Credit History | 15% |

| Credit Mix | 10% |

| New Credit | 10% |

Watch the full (2:27 min) video walkthrough on YouTube →

FACTOR 1 · 35% OF YOUR SCORE

Payment History — The single biggest factor

This is the most heavily weighted element in your score for good reason: lenders want to know, above everything else, whether you pay your bills on time. Every on-time payment builds your score. Every missed or late payment damages it — and that damage lingers on your report for up to seven years. Even one 30-day late payment can drop a good score by 60–110 points.

| 🏡 Realtor Tip: If you’re planning to buy in Fairfield County in the next 6–12 months, set every account to autopay minimum payments today. One forgotten bill can cost you thousands in mortgage interest. |

FACTOR 2 · 30% OF YOUR SCORE

Amounts Owed — Your credit utilization ratio

This factor measures how much of your available revolving credit you’re currently using. It’s expressed as a percentage — if you have a $10,000 credit limit and carry a $3,000 balance, your utilization is 30%. Lenders want to see this number below 30%, and ideally below 10% for the strongest scores. Maxed-out cards are a major red flag, even if you pay them off monthly.

| 🏡 Realtor Tip: Paying down balances before applying for a mortgage is one of the fastest ways to boost your score. Unlike late payments, utilization improvements can show up on your report within 30 days of paying down a balance. |

FACTOR 3 · 15% OF YOUR SCORE

Length of Credit History — Time is on your side

The longer your credit accounts have been open and active, the better. This factor considers the age of your oldest account, your newest account, and the average age of all accounts. This is why financial advisors often caution against closing old credit cards — even ones you no longer use. Closing an old account shortens your average credit age and can ding your score.

| 🏡 Realtor Tip: Don’t close unused credit cards in the months before buying a home. Keep them open with a small recurring charge (like a streaming subscription) paid automatically each month. |

FACTOR 4 · 10% OF YOUR SCORE

Credit Mix — Variety shows responsibility

Lenders like to see that you can manage different types of credit responsibly. A healthy mix includes revolving credit (credit cards), installment loans (auto, student, personal), and ideally a mortgage. You don’t need one of every type — and you should never open new accounts just to diversify. But if you only have credit cards, adding a small installment loan over time can gradually help your mix.

| 🏡 Realtor Tip: This factor matters least in the short term. Don’t make major financial decisions — like taking out a new loan — just to improve your credit mix before buying a home. |

FACTOR 5 · 10% OF YOUR SCORE

New Credit — Every application leaves a footprint

Each time you apply for new credit, the lender performs a “hard inquiry” on your report. One inquiry typically costs you 5–10 points and stays on your report for two years. Multiple applications in a short window — outside of rate shopping for a single mortgage — can signal financial stress to lenders. The good news: mortgage-related inquiries within a 45-day window are typically grouped and counted as just one.

| 🏡 Realtor Tip: Avoid opening any new credit accounts — cards, car loans, store financing — in the 6 months before applying for a mortgage. Even a single new account can raise lender questions at underwriting. |

Frequently Asked Questions

How often is my credit score updated?

Your credit score updates whenever your lenders report new information to the bureaus — typically once a month. This means improvements from paying down balances or making on-time payments can show up relatively quickly, usually within 30–60 days.

Which credit score do mortgage lenders use?

Most mortgage lenders use FICO scores — specifically FICO 2, FICO 4, and FICO 5 — pulled from all three major bureaus (Equifax, Experian, and TransUnion). They typically use the middle of the three scores. This may differ from the score you see on free monitoring apps, which often use VantageScore.

How much can I realistically improve my score before buying?

It depends on what’s holding your score down. Paying off high balances can produce significant improvement in 30–60 days. Clearing up errors through a dispute can take 30–45 days. Recovering from a late payment or collection takes longer — typically 12–24 months of clean history. Most buyers can meaningfully improve their score in 3–6 months of focused effort.

Should I check my own credit report before talking to a lender?

Absolutely — and you should do it at least 3–6 months before you plan to buy. This gives you time to dispute errors, pay down balances, and address any surprises before a lender sees your file. You can access your free report from all three bureaus at AnnualCreditReport.com.

| Want to know where your credit stands before buying in Fairfield, Southport, Westport and beyond? I work alongside William Raveis Mortgage to help buyers understand their credit picture before they ever start touring homes. Reach out and let’s talk about getting you — and your score — ready to compete. |

Linda Raymond, Realtor | 203-912-4440

William Raveis Real Estate | 2525 Post Rd | Southport, CT | 06890

Pingback: How to Compete With Cash Buyers in Fairfield, Southport, and Westport CT— Even With a Mortgage | Fairfield and Westport CT Real Estate Guide