Are we going to face another “2008” after the the failure of Silicon Vally Bank (SVB)?

There are a number of key differences regarding the housing market, consumers, and the banking situation right now compared to that of 2008. Here are six.

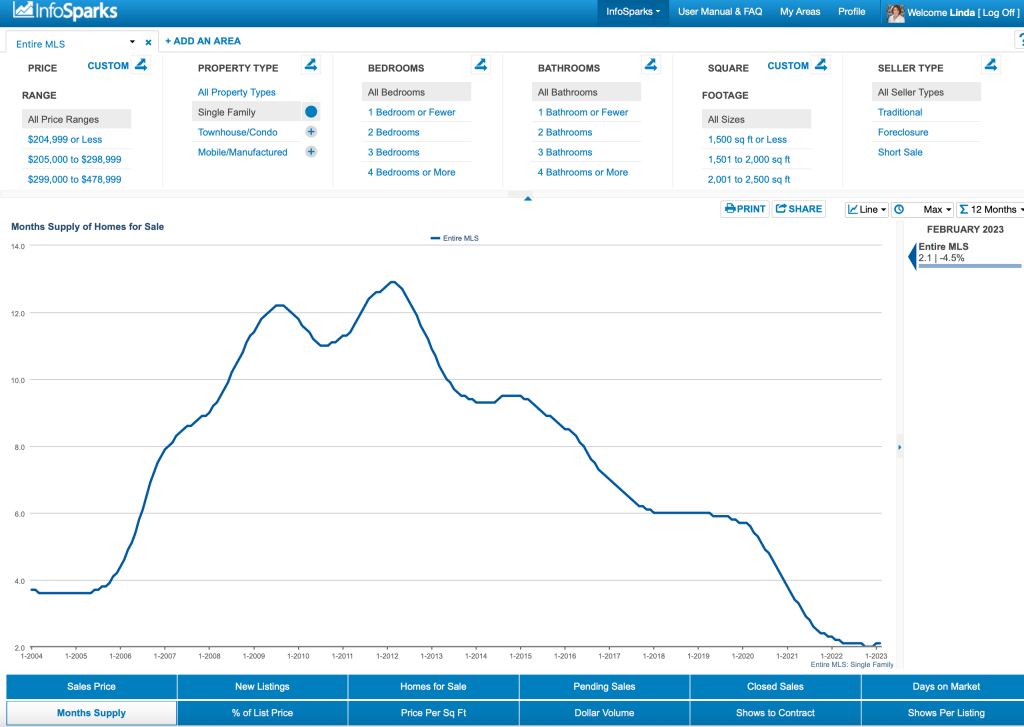

- Inventory is low now, and it was not in 2008. The chart (right) from InfoSparks shows the longterm housing inventory trend and, specifically that here were 9 months of supply in February 2008 and 2 months of supply in February 2023!

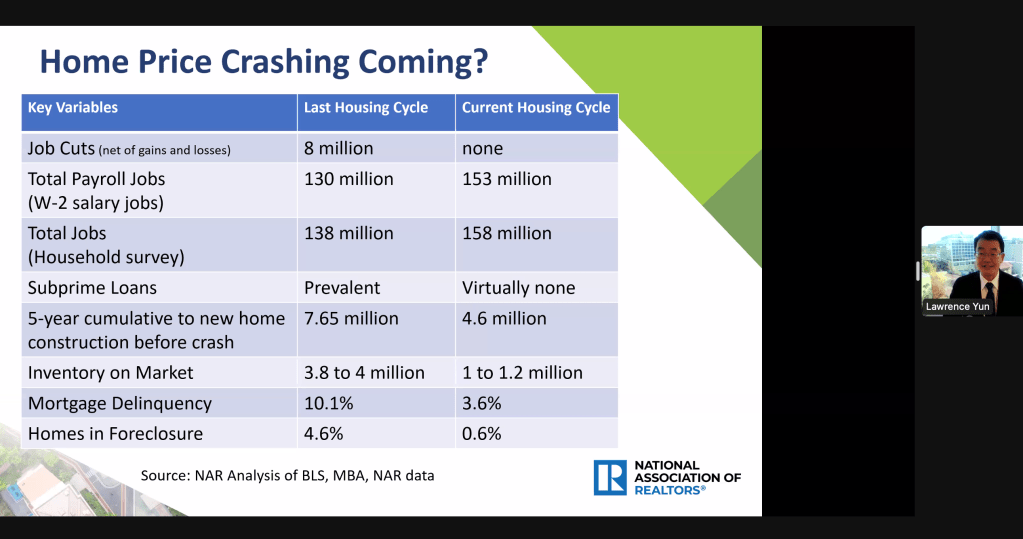

- New construction levels are low now, almost half what they were in 2008. (see table below)

- Mortgage delinquency is low now and it was not in 2008.

- Foreclosure levels are minimal now, and they were not in 2008.

- Subprime loans are virtually non-existent now, but they were prevalent in 2008.

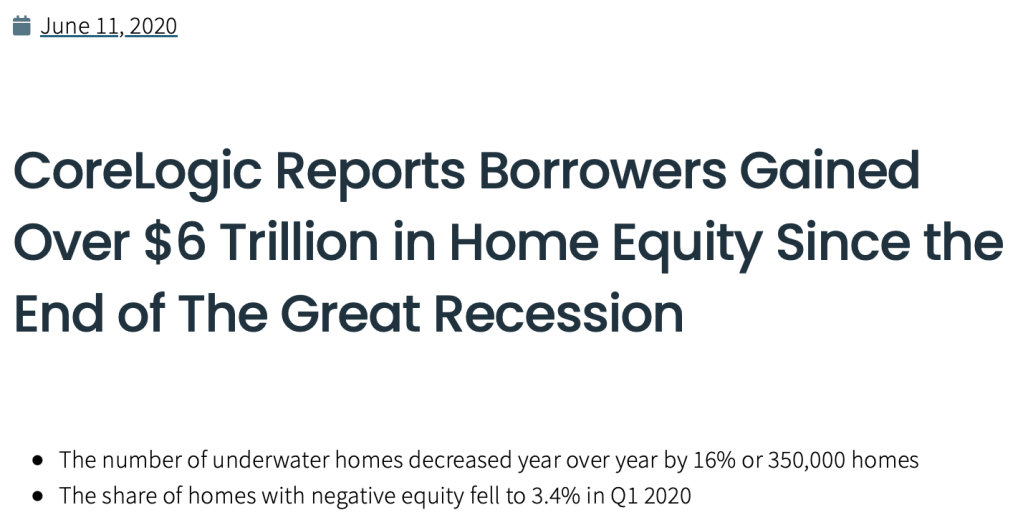

- Homeowner equity is high now, but was negative for many in 2008. (see CoreLogic statement below)

Now, the market, consumer credit scores, and homeowner equity are all much healthier than they were in 2008. Below is an additional summary of key variables from the National Association of Realtors.

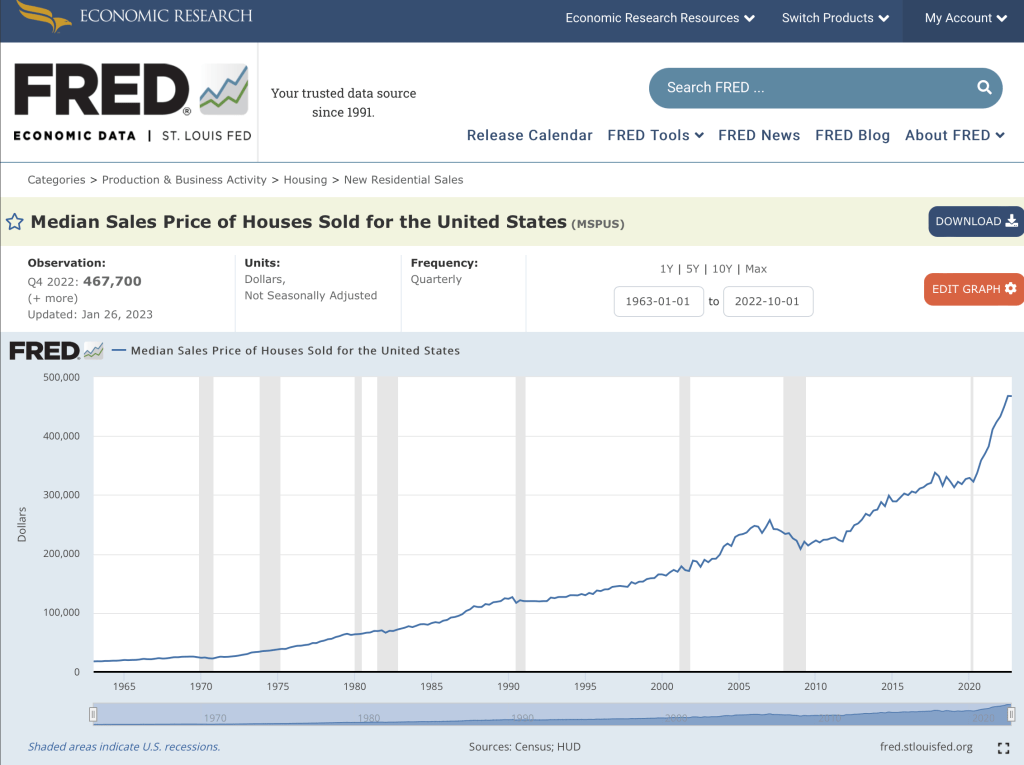

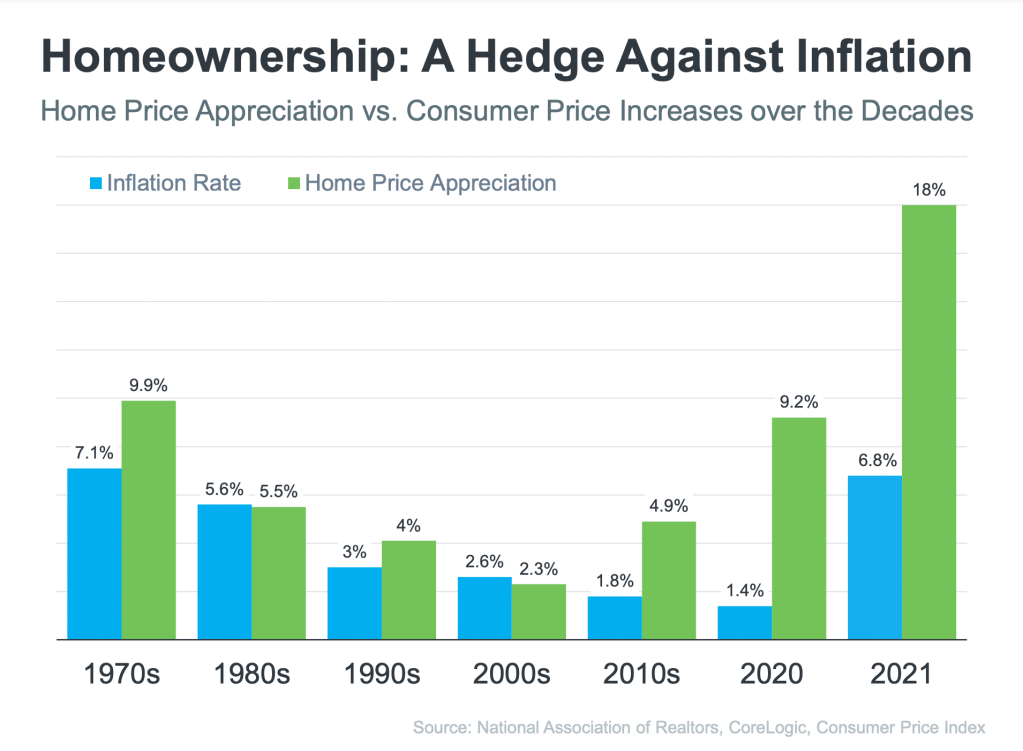

What we do know is that home values appreciate in the longterm and have historically outpaced inflation.

What makes SVB different from the first bank that launched the domino downfall in 2008?

The Silicon Valley Bank is a fraction of the size of the other banks. For example, an article by Troy Palmquist published by Innman says that at the end of 2022, SVB had assets worth about $211 billion, whereas Bank of America had more than $3 trillion at that time. So the scope does not compare. Also, SVB and Signature Bank served a narrow niche within the banking sector compared to the majority of banks that are protected by being significantly more diversified. Most importantly, the most recent stress test implemented by the Federal Reserve demonstrated that major banks could survive both a deep recession and significant unemployment, neither of which are anticipated to be the case.

Should I commit to my plans and embrace the spring market?

Buying and selling your home is an emotional decision. But you now have some strong facts to support your move forward and an improved quality of life, especially if it’s a decision that’s taking you where you want to go! If you want to move forward with your plans, the graphs above show some longterm trends that can support your decision. Below are some resources to help put your plan into action.

How can I bridge the gap between buying and selling when “cash is king” and many markets are still very competitive for buyers?

In competitive markets such as Fairfield, Westport, Southport, and Rowayton, and Darien Connecticut as well as coveted vacation spots like Kennebunkport, Maine, there are still fast-paced sales and multiple-offer situations. Homes are still selling at or above the asking price, and many accepted offers are cash bids with no mortgage contingency.

William Raveis Real Estate offers solutions to get you where you want to go!

Raveis Purchase will enable you to unlock the equity in your current home and make a non-contingent offer on your new one.

Raveis CashBid will buy the home you want to sell and the home you want to buy so that you can accomplish an all-cash transaction and finance later.

So if you want to make a move and overcome some logistical challenges to doing so, reach out and let’s get the conversation started.